- Joined

- Aug 11, 2007

- Messages

- 46,230

- Reaction score

- 27,175

But we're all (most of us at least) part of the global 1%.

I just bought a pair of bootstraps. When I get home I'm going to pull them up ALL NIGHT. By morning I hope to check my investments and see billions

Economic slaves, that is.

While simpletons and intellectual lightweights quibble about race politics, they're too miopic to realize that the great divide is no longer race....it's economic class. The 1% (white, black, yellow, whatever) is content with economically enslaving the 99%, regardless of how much melanin (or lack theroef) in their skin.

A few fun facts for you to ponder:

- The 40 richest people in the world, have more money than the poorest 3.5 BILLION people on the planet.

- Billionaires saw their wealth increase by $762 billion dollars in 12 months, enough to end global poverty 7x over.

- In 2017, 4 out of every 5 dollars of wealth generated, went to the top 1%, leaving the last dollar for the 99%.

- Wealth inequality is REAL, and it's only getting worse. The 1% will have you believe that it's a fair economic playing field for everyone, but that's far from the truth. The game is rigged against YOU, so that you can be farmed for your income, rather than become successful in your own right.

Have a nice day.

Jokes on you. We're all just a pair of bootstraps away from also being billionaires. So I can't be a slave to my future self. Boom, game over.

I just bought a pair of bootstraps. When I get home I'm going to pull them up ALL NIGHT. By morning I hope to check my investments and see billions

Average income in the us is 60000

You work at least 30 years

30 x 60000=1.8 million

Put away your ten percent, should be 15, and you retire a dirty filthy evil millionaire

Then your kids inherit that if you don’t piss it away

THe cycle continues

Boom

Or

Spend every penny you have

Never learn a skill you can market

Stay high

Have multiple kids you can’t afford because it’s your right to queef mouths into the world

Watch six hours of tv a day while saying you don’t have time to go to school or whatever

Die poor or worse yet in debt, Bonus points for taking out a reverse mortgage

That cycle continues

Make threads about evil rich people

And then dumb fucks when confronted with reality say

What about the disabled

What about the fifteen year old girl who has eight kids and dropped out

Etc...

Wish more people had your clarity.

The right-wing, while condemning them publicly, privately thank god every day for the identity politic warriors. Those pathetic, misguided souls are doing more to thwart the class struggle than 20 Koch brother PAC's.

I think the public is right, their position makes absolute sense to me because I see both sides of it. On one hand, I work hard to build my small business and my wife does the same. We mostly live within the means of our own sweat equity. OTOH, I went to a very good college and I went to law school. And my classes were filled with very smart, very hard-working people who work long hours chasing the American dream and they will not end up anywhere near my net worth for reasons that have nothing to do with character stuff that gets thrown around.

I know teachers who toiled for 15 years before they cracked $100k year. I know people with Master's degrees in engineering who barely make $60k. And I know guys who make $250k+. I know lawyers who 10 years out are struggling to build a sustainable practice, doing doc review year in, year out. In all honesty, hard work has nothing to do with why one of them makes more money than the other.

So, smart financial habits and decisions are fruitful in the long run but it's fallacious when people suggest, overtly or subtly, that the difference between the guy who's struggling to make ends meet and the guy who's stacking $150k/yr is in any way purely reflective of their effort or their character.

I didn't appreciate this when I was younger. I assumed you go out work hard and eventually you stack chips. The reality is different. You go out and work hard and you stack what you're paid but the line between doing okay and doing really well is not easy to find or cross. And by the time, most people are facing the reality that their education and career choices aren't going to result in economic freedom so much time has been lost that it's nigh impossible to chart a new path.

I don't think many people realize just unprepared they are for ever really retiring. THey're so busy pointing to the alleged failings of those with less than them that they don't realize just how far they are themselves from the type of financial independence they claim they want. And the truth is, 90% of the population will never get there even if they make all of the right decisions because the math doesn't work in their favor.

I think the public is right, their position makes absolute sense to me because I see both sides of it. On one hand, I work hard to build my small business and my wife does the same. We mostly live within the means of our own sweat equity. OTOH, I went to a very good college and I went to law school. And my classes were filled with very smart, very hard-working people who work long hours chasing the American dream and they will not end up anywhere near my net worth for reasons that have nothing to do with character stuff that gets thrown around.

I know teachers who toiled for 15 years before they cracked $100k year. I know people with Master's degrees in engineering who barely make $60k. And I know guys who make $250k+. I know lawyers who 10 years out are struggling to build a sustainable practice, doing doc review year in, year out. In all honesty, hard work has nothing to do with why one of them makes more money than the other.

So, smart financial habits and decisions are fruitful in the long run but it's fallacious when people suggest, overtly or subtly, that the difference between the guy who's struggling to make ends meet and the guy who's stacking $150k/yr is in any way purely reflective of their effort or their character.

I didn't appreciate this when I was younger. I assumed you go out work hard and eventually you stack chips. The reality is different. You go out and work hard and you stack what you're paid but the line between doing okay and doing really well is not easy to find or cross. And by the time, most people are facing the reality that their education and career choices aren't going to result in economic freedom so much time has been lost that it's nigh impossible to chart a new path.

I don't think many people realize just unprepared they are for ever really retiring. THey're so busy pointing to the alleged failings of those with less than them that they don't realize just how far they are themselves from the type of financial independence they claim they want. And the truth is, 90% of the population will never get there even if they make all of the right decisions because the math doesn't work in their favor.

So the public's disposition of persecuting the wealthy is a productive, fruitful, or even rightful one?

I read your points but I think there are tremendous gaps between people's financial knowledge and practices;

here in lies the key difference between the wealthy and your everyday Joe or those prepared and unprepared for retirement.

-Sure many variables come into play; previous family wealth, alumni aiding your acceptance in a prominent university, a bit of luck in investments, the rare occasion of developing & selling something truly valuable, etc.

But rather than an environment of whining and begging for more tax on the rich; isn't the real problem individual life choices and individual taxation of the middle and lower class?

Sound financial practices, if not for your lifetime, but for your future generations... isn't this a much smarter idea.

Where has personal accountability gone?

Is it not more fruitful for individuals to learn financial education early on; how to spend, save, invest, and manage your money? What about parents not just verbalizing it but enforcing positive spending habits?

What about picking a college degree with the higher salary?

(teachers and social science degrees are notorious for not providing large incomes)

What about investing in oneself and making sure your skills and resume continue evolving?

While you may agree with the current dynamic, I see a crab culture where misery(high taxation and difficult financial times for many americans) enjoys company(attempts to tax the wealthy even more because our financial standing isn't where we would like it).

Just remember it's tough to wish for better financial standing while still voting democrat and their respective large gov't, high taxation approach.

The hopelessness is rather sad at this point.

NOTE

I harp on taxes because it is easily the largest income extractor(when you factor in current income tax rates and the fact employers have to spend money on high payroll tax as opposed to paying a portion of that same money towards employees)

Average income in the us is 60000

You work at least 30 years

30 x 60000=1.8 million

Put away your ten percent, should be 15, and you retire a dirty filthy evil millionaire

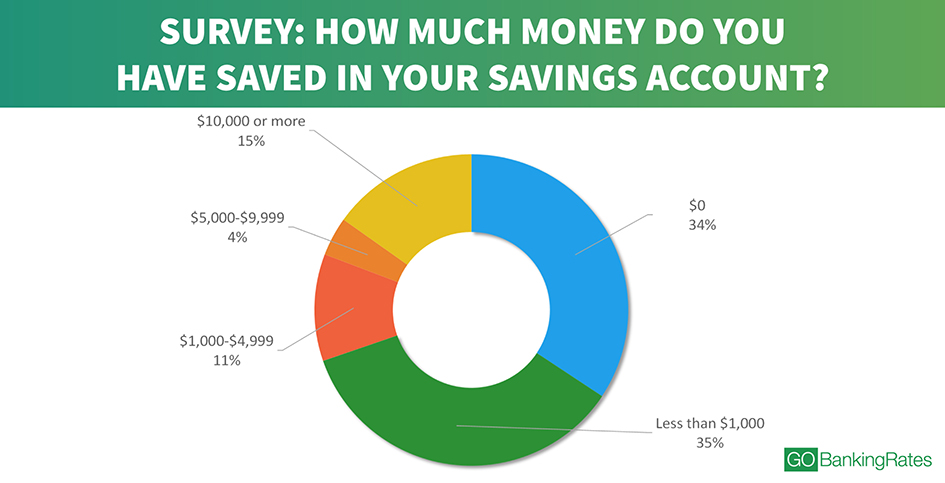

You’re a miserable person and deserve to be poor1.The average household income in Murka is skewed by wealth inequality and extremes of the .001%

2.Apparently in your alternate universe this median household has 0 expenses and can just tuck all that income away in savings.

3. Your math sucks

Yeah, I remember that time when things were so much better...Economic slaves, that is.

While simpletons and intellectual lightweights quibble about race politics, they're too miopic to realize that the great divide is no longer race....it's economic class. The 1% (white, black, yellow, whatever) is content with economically enslaving the 99%, regardless of how much melanin (or lack theroef) in their skin.

A few fun facts for you to ponder:

- The 40 richest people in the world, have more money than the poorest 3.5 BILLION people on the planet.

- Billionaires saw their wealth increase by $762 billion dollars in 12 months, enough to end global poverty 7x over.

- In 2017, 4 out of every 5 dollars of wealth generated, went to the top 1%, leaving the last dollar for the 99%.

- Wealth inequality is REAL, and it's only getting worse. The 1% will have you believe that it's a fair economic playing field for everyone, but that's far from the truth. The game is rigged against YOU, so that you can be farmed for your income, rather than become successful in your own right.

Have a nice day.

Your first paragraph essentially disregards what I said. It's not an world where people aren't making smart financial decisions and then complaining about results. It's a world where even when they make smart financial decisions, the system is not designed to help them maximize that.

Most of your post is an example of exactly what I said is the problem - the assumption that it's a lack of money management efforts or other character related failings that are in play, like "personal accountability". I said the opposite - that personal accountability isn't enough to offset the changes that are being made in the system overall.

You mention democrats as if that has anything to do with it. It's not democrats demanding that we reduce immigrant labor to protect American labor wages. Or that we protect the incomes of the coal industry or other outdated industries. The partisan angle is a red herring thrown around when people don't want to face all of the wealth protecting demands from both sides of the aisle.

People cry about the "current environment", usually with some reference to past accountability. The tax rates of the top 0.1 and 0.01 percent of taxpayers have dropped substantially since the 1950s. The average tax rate on the 0.1 percent highest-income Americans was 50.6 percent in the 1950s. The average tax rate on the top 0.01 percent was 55.3 percent in the 1950s.

Those rates have dropped significantly.

Wages have not risen with productivity since the 1970's. The minimum wage, adjusted for inflation, has been dropping since 1968. <--- That's the money your average American makes for working.

Meanwhile the rate on long term capital gains has dropped from 25% to 15%. <--- That's the money that your average American puts aside because they don't need it to pay bills.

So, money for working has decreased. Tax savings for money you don't need to live on has increased. Taxes on the upper end have decreased. The amount of money from the benefitting group is directly impacted by the money in the detrimental group. If people make less money for working then they have less money for investing, no matter how good they are with managing their money.

So, personal accountability and money management doesn't have anything to do with this conversation. The "current environment" has shifted more and more benefits away from working for a living and towards the money that people don't need.

Only the economically naive would ignore that, even if they're benefitting from it. Someone can say "I like the current system" but they can't say "Well this system treats the average American worker just as well as the previous system and the only thing that has changed is the average American's sense of personal accountability."

I generally support the current system (to an extent) because entrenches more and more of the wealth that my parents and my in-laws put together. I don't understand how people who don't have at least $500k in stocks/bonds (miss me with that home equity bullshit) can say the same. I mean, I get the point of being aspirational but it's usually coupled with a complete lack of knowledge about how the economy has evolved for your average American.